Oahu’s Industrial Market: Resilience and Opportunity

Oahu’s industrial market defies national trends with tightening vacancies, rising absorption, and strong investor demand. New developments and steady rents highlight a resilient sector poised for growth despite economic uncertainties. Dive into the full market update.

Industrial Market Trends: Oahu’s Resilience in Focus

Industrial market trends continue to define Oahu’s commercial real estate landscape, with Q3 2025 underscoring the sector’s remarkable resilience. Despite national headwinds and a softening in broader industrial markets, Oahu’s fundamentals remain robust. Vacancy rates have tightened, net absorption has rebounded, and investor interest is holding strong. This update unpacks the latest data, analyzes submarket performance, and highlights the strategic opportunities shaping Oahu’s industrial future.

Oahu Industrial Market: Strong Recovery and Resilient Demand

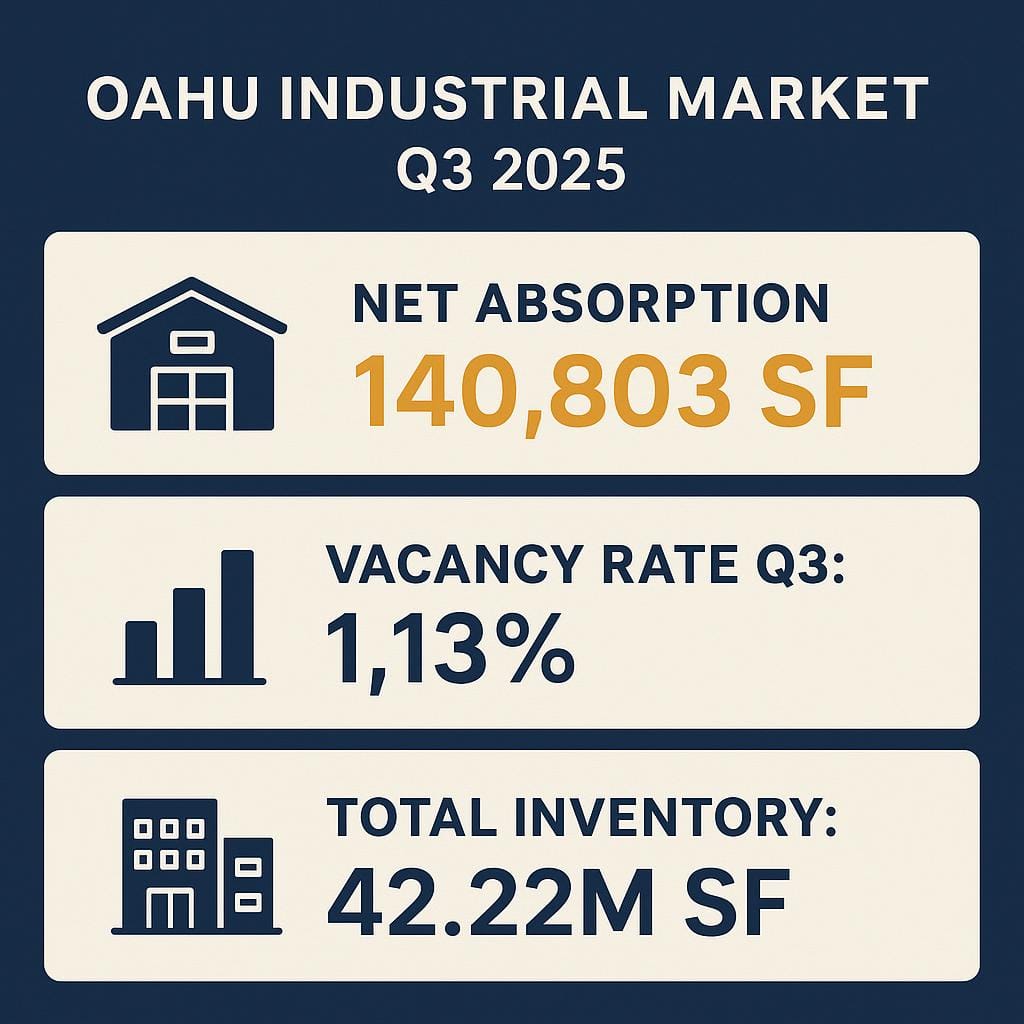

The Oahu industrial market demonstrated a significant recovery in Q3 2025, with net absorption surging to 140,803 square feet—a sharp reversal from two consecutive quarters of negative absorption. This positive momentum reflects renewed tenant confidence and a tightening supply environment. The vacancy rate dropped to 1.13% from 1.47% in Q2, marking one of the lowest levels nationwide. This contraction in available space is a direct result of robust demand from logistics, construction, and wholesale sectors, all seeking strategically located industrial assets. The total industrial inventory now stands at 42.22 million square feet, with new supply struggling to keep pace with market needs. These dynamics reinforce Oahu’s reputation as a supply-constrained, high-demand market, where net absorption trends are a key barometer of sector health.

- Vacancy Rate: 1.13% (down from 1.47%)

- Net Absorption: 140,803 SF (positive after two negative quarters)

- Inventory: 42.22 million SF

Industrial Rental Prices: Navigating a Tight Leasing Environment

Industrial rental prices in Oahu remain elevated, reflecting the ongoing shortage of quality space. The average asking rent moderated to $1.56 per square foot per month in Q3, down from a record high of $1.65/SF in Q2. Despite this slight decrease, rents are still among the highest in the region, underpinned by persistent demand and limited new supply. Operating expenses have also climbed, rising 9.8% over the past three quarters to $0.56/SF/month. This increase is driven by higher insurance premiums, property taxes, wage adjustments, and construction costs—expenses typically passed through to tenants via NNN leases. For occupiers, these cost pressures mean that total occupancy costs are rising, even if base rents have temporarily plateaued. Understanding the interplay between rental rates and operating expenses is crucial for both landlords and tenants navigating lease negotiations in this competitive environment.

- Average Asking Rent: $1.56/SF/month (down from $1.65/SF)

- Operating Expenses: $0.56/SF/month (up 9.8%)

Industrial Development Projects: Pipeline and Construction Outlook

Oahu’s industrial development projects are accelerating to address chronic supply shortages. In Q3 2025, 134,194 SF of new industrial space was delivered, with several major projects—such as Coral Creek Center and Alexander & Baldwin’s 121,000 SF Kapolei warehouse—progressing rapidly. Looking ahead, over 570,000 SF of new inventory is projected by the end of 2026, signaling a robust construction pipeline. Year-to-date construction permit volume reached $1.33 billion (a 38.75% year-over-year increase), highlighting developer confidence and strong capital inflows. The surge in YTD construction permits demonstrates the market’s commitment to expanding capacity, though geographic and regulatory constraints continue to limit the pace of new supply. For investors and occupiers, monitoring YTD construction permits and the timing of project deliveries will be critical in anticipating future shifts in market balance.

- New Supply Delivered (Q3): 134,194 SF

- Projected New Inventory by 2026: 570,000+ SF

- YTD Construction Permit Volume: $1.33B (up 38.75% YOY)

Submarket Performance: Key Insights Across Oahu

Submarket performance across Oahu reveals nuanced trends in industrial vacancy rates and rental pricing. The Honolulu submarkets—including Iwilei, Kalihi, Airport, and Mapunapuna—posted a collective vacancy rate of just 0.97% and average asking rents of $1.48/SF/month. Central Oahu (Halawa, Pearl City/Aiea, Waipahu) outperformed with the lowest vacancy at 0.74% and the highest average rent at $1.78/SF/month. In contrast, Windward Oahu (Kapaa, Kaneohe) recorded the highest rents, ranging from $2.45 to $3.00/SF/month MG, but also saw a higher vacancy rate of 3.8%. West Oahu (Campbell, Kapolei) experienced mixed results, with Kapolei Business Park’s vacancy rising to 2.02% and Kalaeloa Industrial’s vacancy spiking to 28.01% due to a large block of available space. These variations underscore the importance of submarket performance analysis for investors and occupiers seeking to optimize their industrial real estate strategies.

- Honolulu: 0.97% vacancy, $1.48/SF/month

- Central Oahu: 0.74% vacancy, $1.78/SF/month

- Windward Oahu: 3.8% vacancy, $2.45–$3.00/SF/month MG

- West Oahu: Kapolei Business Park 2.02% vacancy, Kalaeloa Industrial 28.01% vacancy

Impact of Construction on Industrial Vacancies: Economic Forecast and Strategy

The impact of construction on industrial vacancies remains a focal point as Oahu approaches a forecasted mild recession by 2026. Despite broader economic uncertainty, the industrial sector is projected to maintain a sub-2% vacancy rate, with modest rent growth expected through 2025. This resilience is driven by persistent supply constraints, geographic limitations, and ongoing demand from logistics and wholesale sectors. The 2025 recession impact on Oahu industrial market is anticipated to be less severe than on the mainland, thanks to the island’s unique supply-demand dynamics. However, stakeholders should remain vigilant regarding macroeconomic risks, including inflation, immigration policy shifts, and potential slowdowns in tourism and construction. Strategic planning around new developments, lease renewals, and capital allocation will be essential for navigating the evolving landscape.

- Forecasted Vacancy Rate (2025–2026): Sub-2%

- Key Demand Drivers: Logistics, wholesale, and construction sectors

- Economic Risks: Mild recession, inflation, policy changes

Investment Opportunities: Positive Sentiment Amid National Shifts

Investment opportunities in Oahu’s industrial sector remain compelling, even as national commercial real estate markets face rising vacancy rates and slowing rent growth. Investor sentiment is buoyed by the island’s chronic supply constraints, steady tenant demand, and the proven stability of industrial assets. Year-to-date industrial sales volume reached $8.33 billion (as of May 2025), with contracting sales at $2.89 billion and wholesale sales up 11.84% year-over-year to $5.29 billion. These figures highlight ongoing capital flows and acquisition activity, particularly for well-located, high-quality assets. While national industrial vacancy rates have climbed to 7.3% and rent growth is projected to slow to 0.5–1% in 2025, Oahu’s market remains insulated by its unique fundamentals. For investors seeking portfolio stability and long-term value, Oahu’s commercial real estate landscape offers a rare combination of resilience and upside potential.

- YTD Industrial Sales Volume: $8.33B (May 2025)

- Contracting Sales (YTD): $2.89B

- Wholesale Sales Growth: 11.84% YOY ($5.29B)

- National Vacancy Rate: 7.3% (Oahu remains below 2%)

Conclusion: Oahu’s Industrial Market Trends Signal Enduring Strength

Oahu’s industrial market trends in Q3 2025 showcase a sector defined by resilience, ongoing demand, and robust investment potential. With vacancy rates near historic lows, a healthy development pipeline, and strong investor confidence, the market stands out as a stabilizing force in Hawaii’s commercial real estate landscape. As the island navigates broader economic uncertainties, its industrial sector remains well-positioned to deliver value for landlords, tenants, and investors alike. Colliers Hawaii’s deep local expertise and commitment to client success ensure that stakeholders are equipped to capitalize on the unique opportunities this dynamic market presents.